Master of Science in Accounting

Posted on December 31st, 2020 by admin in Bookkeeping | No Comments »

This leads to inaccurate financial reporting where data is misrepresented and this misleads stakeholders, regulators, and auditors leading to potential risks of non-compliance, legal action, and loss of trust. Accounting involves recording, classifying, organizing, and documenting financial transactions and data for internal tracking and reporting purposes. Businesses of all sizes use accounting to remain legally compliant and measure balance sheet and assess their financial health. The professionals who lead these efforts possess deep, detailed technical proficiencies often developed through a bachelor’s degree program in accounting.

What career opportunities can I pursue with a certificate in accounting?

Accounting software does a lot of the heavy lifting (such as keeping track of debits and credits) for you. However, it’s still important to understand basic accounting principles to know what’s happening behind the scenes. Business owners should be able to enter transactions, reconcile accounts and interpret financial statements accurately. This type of accounting involves an independent review of a company’s financial statements to ensure that they are accurate and in compliance with generally accepted accounting principles (GAAP).

Learn About Bloomberg Tax

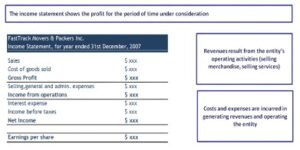

This is the practice of recording and reporting financial transactions and cash flows. This type of accounting is particularly needed to generate financial reports for the sake of external individuals and government agencies. These financial statements report the performance and financial health of a business. For example, the balance sheet reports assets and liabilities while the income statement reports revenues and expenses.

Accounting information systems

- When businesses analyze historical transaction data they can forecast future cash flow and mitigate risks enabling informed decision-making.

- The reconciliation reports need to be reviewed thoroughly and if any discrepancies are found it needs to be adjusted to match the differences.

- U.S. public companies are required to perform financial accounting in accordance with generally accepted accounting principles (GAAP).

- The CFE credential is recognized and respected by businesses, governments, and law enforcement agencies worldwide.

- Tax accountants may also be involved in tax planning and advising clients on how to structure their affairs.

With the flexibility of a field like accounting, expect the same with program options. Whether it’s a certificate you’re pursuing or a graduate degree, you have options for online, on-campus, or hybrid education. For example, the current ratio compares the amount of current assets with current liabilities to determine how likely a company is going to be able to meet short-term debt obligations. This may influence which products we review and write about (and where those products appear on the site), but it in no way affects our recommendations or advice, which are grounded in thousands of hours of research.

Understanding Accounting

This rule applies to expenses and income such as salaries, sales, purchases and commissions. This rule is applicable to transactions involving people or businesses, for instance, a bank transaction. This rule is applicable to the assets of a business, such as cash, land, building, equipment, furniture, etc. A CPA, or “Certified Public Accountant”, is recognized in the accounting field. It is a designation https://www.bookstime.com/ that is considered challenging to obtain, with exact requirements varying from state to state. However, upon receiving the designation, a CPA is considered an expert in the field of accounting, and would typically enjoy a much higher salary than that of an accountant.

What Is the Main Purpose of Financial Accounting?

- Intercompany transactions are important for accurately reporting the financial relationship and exchanges between two different companies within the same corporate group.

- Their primary job is to help clients with their taxes so they can avoid paying too much or too little in federal income or state income taxes.

- This rule is applicable to transactions involving people or businesses, for instance, a bank transaction.

- In addition to this financial overview, proper accounting practices prepare your business to file taxes and produce financial statements needed for potential investors or business loan applications.

- Businesses must account for overhead carefully, as it has a significant impact on price-point decisions regarding a company’s products and services.

- Government accounting may have various challenging and interesting work assignments.

With 600+ scholarships to choose from, this is one of the best ways to lower your bookkeeping for cleaning business college costs. Explore programs of your interests with the high-quality standards and flexibility you need to take your career to the next level. Explore how an accounting certificate can give you the skills you need without a large upfront commitment. Many, or all, of the products featured on this page are from our advertising partners who compensate us when you take certain actions on our website or click to take an action on their website.